As the founder and broker of Tverdov Housing, with over a decade specializing in New Brunswick's real estate—particularly multi-family investments and homes near Rutgers University—I've helped many self-employed buyers, from freelancers to business owners, successfully purchase properties in this Rutgers-driven market. Self-employment offers flexibility but can complicate mortgage qualification due to variable income and tax deductions. With the right preparation, however, buying here is very achievable.

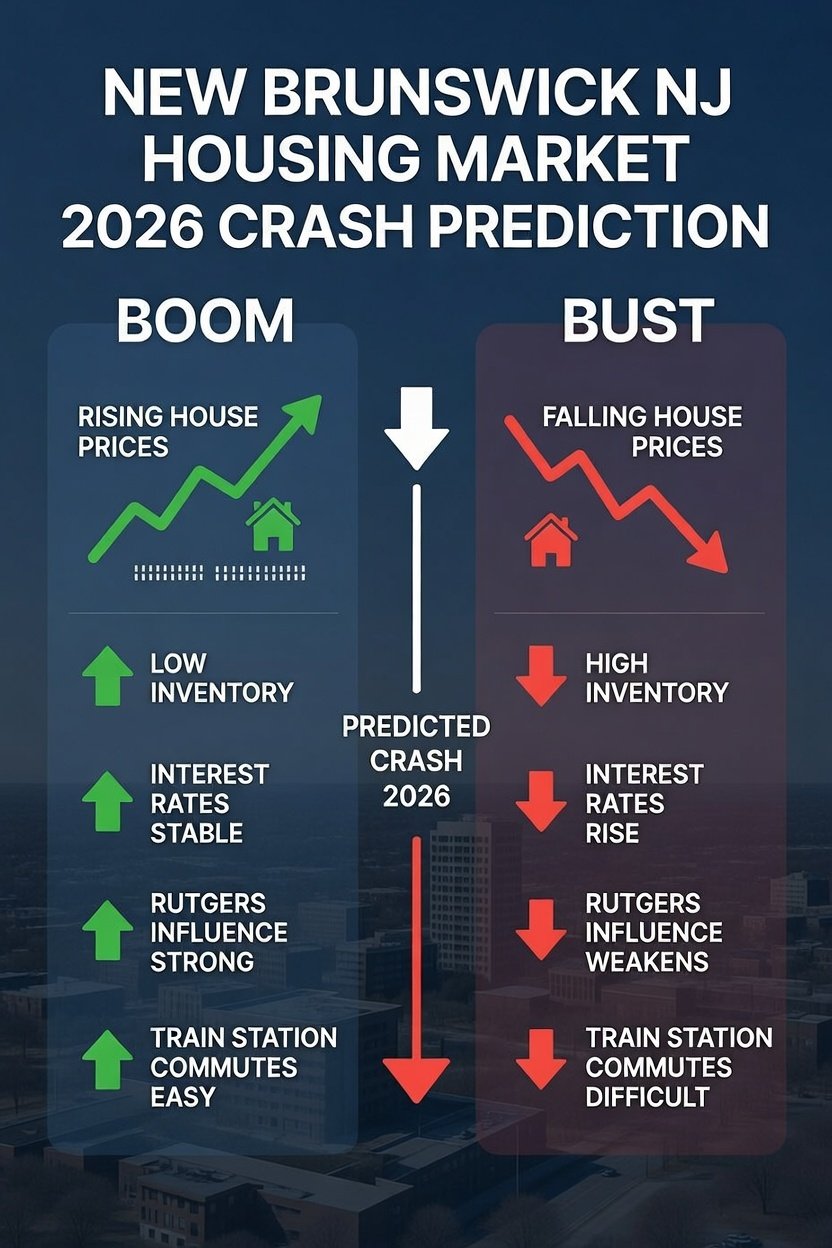

As of January 2026, New Brunswick's market is somewhat competitive (Redfin score around 47/100), with median prices near $433,000-$440,000 and homes taking 70-80 days to go pending. Demand remains strong from university and hospital professionals, making it attractive for self-employed buyers seeking rental income potential.

Key considerations for self-employed buyers:

- Mortgage Qualification: Lenders typically require at least two years of self-employment history in the same field, along with two years of tax returns (personal and business), profit/loss statements, and bank statements. Income is calculated after deductions, so aggressive write-offs can lower your qualifying amount—plan ahead with your accountant. Exceptions exist: Some lenders accept one year if you have prior related W-2 experience.

- Loan Options: Conventional loans are possible with strong credit (often 620+), but many self-employed buyers opt for alternatives:

- Bank statement loans: Use 12-24 months of deposits to verify income (no tax returns needed).

- Non-QM loans: Flexible for fluctuating income, though with higher rates or larger down payments (15-20%). Current 30-year fixed rates hover around 6%, competitive for qualified borrowers.

- Down Payment and Assistance: Expect 3-20% down, depending on the loan. New Jersey's NJHMFA programs are available to self-employed buyers meeting first-time buyer criteria (no home ownership in 3 years) and income limits. The Down Payment Assistance Program offers up to $15,000 (forgivable after 5 years), combinable with other aid for totals up to $22,000 for first-generation buyers.

- Local Tips: Focus on properties with rental potential near campus or the train station to offset costs. New Brunswick requires Certificate of Continued Occupancy (CCO) inspections—factor in potential repairs.

Start early: Get pre-approved with a lender experienced in self-employed borrowers, gather documentation, and partner with a local agent. At Tverdov Housing, we connect clients with trusted lenders and navigate these nuances daily.

For more on Central Jersey strategies, listen to The New Jersey Real Estate Investor podcast.

Ready to buy in New Brunswick? Contact Tverdov Housing—we're experts at making self-employed homeownership a reality here.